Do I need to be a registered investment adviser to build a stock recommendation app?

If your app gives personalized recommendations to buy or sell specific securities, tailored to the income, holdings, or risk tolerance of an individual user, then in the United States that activity is investment advice under the Investment Advisers Act of 1940. The person or company providing it is an investment adviser and generally must register with the SEC or a state securities regulator before operating. A general, non-personalized stock information tool can instead fall under the publisher exclusion recognized in Lowe v. SEC. The dividing line is personalization.

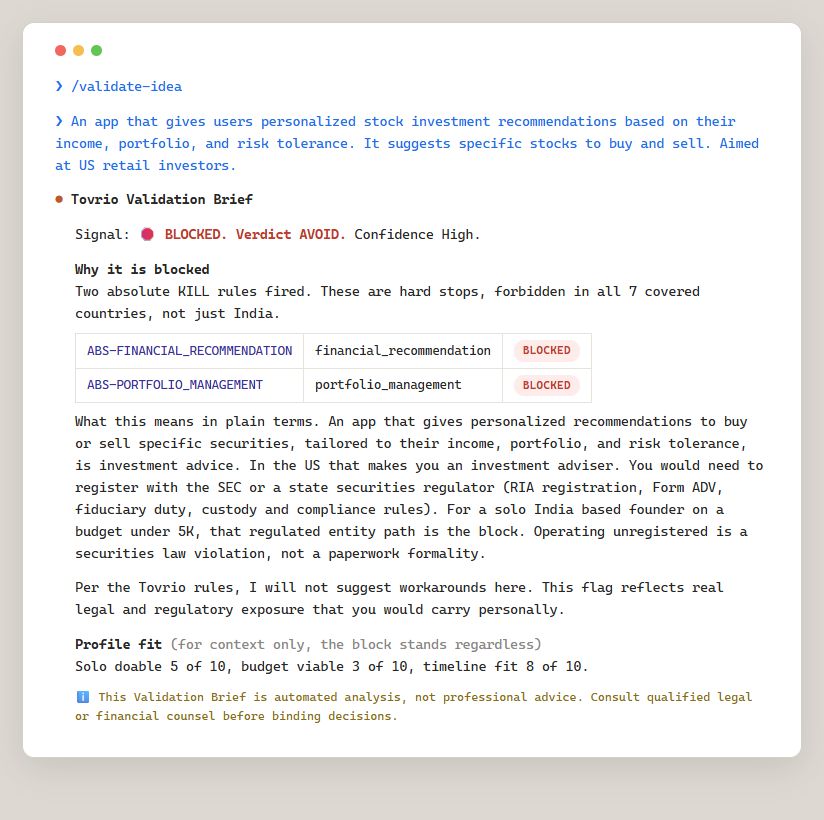

The card above is a real result from a compliance check. The idea tested was a synthetic example: an app that gives users personalized stock picks based on their income, portfolio, and risk tolerance, aimed at US retail investors. The profile was a solo founder outside the US on a small budget. The result was a blocked signal, for the reasons below.

What counts as investment advice versus general financial information?

Investment advice means advising a specific person on the value of securities or on the advisability of buying or selling them. General financial information means publishing facts or analysis for a broad audience without tailoring it to the situation of any one reader. The first is regulated. The second often is not.

| General financial information | Investment advice | |

|---|---|---|

| Example | A page explaining what a price to earnings ratio means, or a market summary written the same for all readers | An output telling a specific user to buy 50 shares of a named stock based on the income and risk profile of that user |

| Personalization | None. Same for everyone | Tailored to the financial situation of the individual |

| Typical US status | May qualify for the publisher exclusion (Lowe v. SEC) | Regulated as an investment adviser under the Advisers Act of 1940 |

Why personalized recommendations make you an investment adviser

Under the Investment Advisers Act of 1940 you are an investment adviser if three elements are met. You provide advice about securities. You do it for compensation. You do it as a business. A stock app that charges for personalized buy or sell calls meets all three. The "for compensation" element is read broadly. A free app that plans to charge later, or that benefits indirectly, can still meet it, so being free today doesn't by itself put a personalized stock app outside the rule. Registration isn't a one-time form. It brings ongoing duties: filing Form ADV, a fiduciary duty to clients, recordkeeping, a written compliance program, and custody rules where they apply.

Source: Investment Advisers Act of 1940, 15 U.S.C. 80b.

The Lowe v. SEC publisher exclusion, and why an AI stock picker probably does not qualify

In Lowe v. SEC the Supreme Court held that impersonal investment advice delivered through a bona fide publication of general and regular circulation is excluded from adviser registration. The key word is impersonal. A newsletter that gives the same analysis to every subscriber can qualify. The exclusion is lost the moment the advice is tailored to the financial situation of an individual.

An AI tool that takes in the income, holdings, and risk tolerance of a user and returns specific trades is, by design, personalized. Whether dynamic, individualized output from a language model can ever count as a publication of general and regular circulation is unsettled. What is clear is that personalization is what pulls a product across the line, and most stock recommendation apps are built to personalize.

What changed in 2025: the Internet Adviser Exemption

On March 27, 2024 the SEC amended the Internet Adviser Exemption under Rule 203A-2(e), and the compliance date was March 31, 2025. The amendment removed the old de minimis allowance that had let an internet adviser also serve up to 15 non-internet clients. Two practical effects for builders. First, an adviser relying on this exemption must now advise all clients exclusively through an operational interactive website at all times. Second, the small client allowance that founders used for friends and family testing is gone, so that quiet testing phase is no longer shielded.

One caution so this is not misread: this exemption governs which regulator you register with, the SEC instead of the states. It doesn't decide whether you must register at all. If you give personalized securities advice, the registration question is already answered.

Source: SEC press release 2024-42.

Does being a non-US founder change the answer?

Not in the way most founders hope. US securities law generally reaches advisers who provide advice to US persons or who use US channels, regardless of where the founder is located. If you open a personalized stock recommendation app to US retail investors, you can trigger US registration requirements even when you and your company sit outside the United States. Where you incorporate doesn't move that obligation off your plate. Confirm your exposure with a securities attorney before you open access to US users.

If you are a solo founder on a small budget

For a solo founder on a small budget, the registration path itself is usually the wall. Form ADV, fiduciary duty, a written compliance program, and custody rules are built for regulated firms, not weekend projects. That is why a compliance check returns this idea as blocked for that profile. It's not that the idea is wrong. It's that the regulated entity path is out of reach at that scale.

These next options are not workarounds that make the blocked idea compliant. They are different products that avoid the regulated activity entirely:

- Build a tool for licensed advisers as a B2B product, rather than advising retail users yourself.

- Ship a general, non-personalized information product that stays inside the publisher exclusion.

- Partner with a registered investment adviser who already carries the license.

Each of these keeps you out of the specific activity that requires registration.

How to validate before you build

The result shown above came from Tovrio, a compliance check that runs an idea against country-specific rules before you write code. The idea tested was a synthetic case, not a real user. The result was a blocked signal with the reasons named here.

This is a validate-before-you-build signal, not legal advice. A flag means "go confirm this with a securities professional before you commit," not "your specific plan is definitely unlawful." You can run your own idea through it.

Frequently asked questions

Does an AI stock picker fall under the Lowe v. SEC publisher exclusion if it is not personalized?

Possibly, if it is genuinely impersonal and delivered to a general audience like a newsletter. The exclusion is for publications of general and regular circulation. The moment the tool tailors output to the financial situation of an individual user, it generally loses the exclusion and looks like investment advice.

If my app gives stock scores from AI sentiment analysis, is that investment advice?

It depends on personalization and framing. A single sentiment score shown the same way to everyone leans toward general information. A score paired with a tailored recommendation to buy or sell for that specific user leans toward investment advice. Borderline designs should be confirmed with a securities attorney.

Can I build a SaaS that mirrors famous investor portfolios without a license?

Copying public holdings into a general, non-personalized feed is closer to information. Telling a specific user to put their money into those positions based on their profile is closer to advice and can require registration. Routing the trades or managing the money directly raises further licensing questions.

Do I need a license to build a stock recommendation app if I am not in the US?

Quite possibly yes. US adviser rules generally apply when you advise US persons, regardless of where you are located. Serving US retail investors can trigger US registration even for a non-US founder.

Does a free stock recommendation app avoid investment adviser rules?

Not necessarily. The for-compensation element under the Advisers Act is read broadly. A free app that plans to charge later, or that earns indirectly, can still meet it. Being free today does not by itself place a personalized stock recommendation app outside adviser regulation.

What is the difference between providing financial information and investment advice?

Financial information is general and the same for every reader. Investment advice is applied to the situation of a specific person. The first can qualify for the publisher exclusion. The second is regulated under the Investment Advisers Act of 1940.

Run your own idea through Tovrio before you build. See how it works.